You've just packed a parcel. Whether it contains an e-commerce product, a valuable gift, or a crucial document, one question hangs in the air: "What if it never arrives?" In the world of shipping, uncertainty is the norm. But resignation should not be.

The biggest financial mistake shippers make is trusting the "basic" insurance included by carriers (regardless of your business). It's an illusory safety net. The only real protection for your goods isad valorem insurance. Still hesitating? Here are 7 compelling reasons that will transform your view of shipment security.

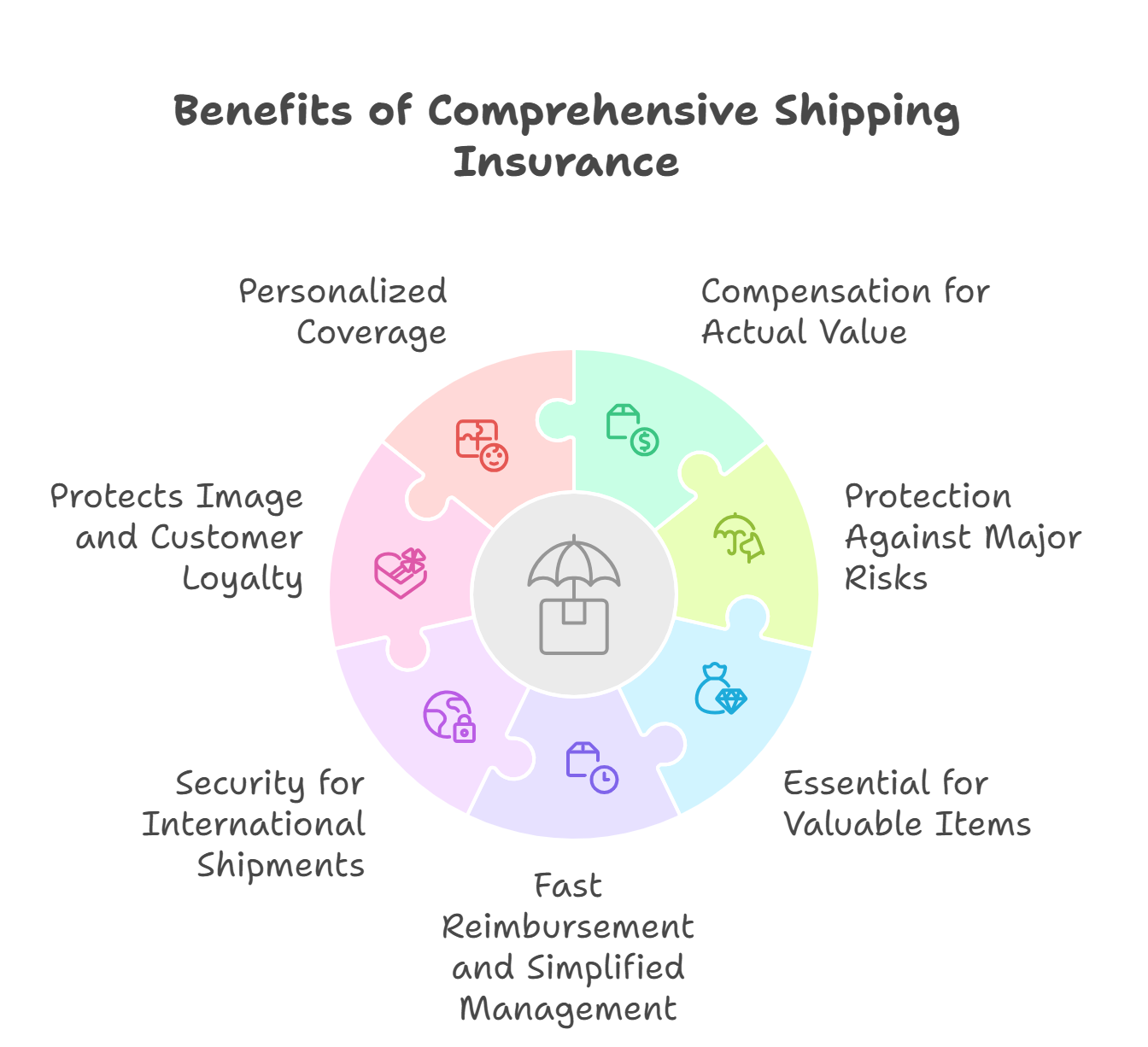

Carriers are liable for between €23 and €33 per kilogram, which means that for a light but high-value parcel, compensation may be significantly less than the actual value of the parcel.

What is Ad Valorem Insurance? (And Why It's NOT an Option)

Before diving into the reasons, let's understand what we're talking about:

- Standard insurance (Carrier): This compensates you based on weight. A derisory flat rate (often ~€23/kg) that takes absolutely no account of what is in your box.

- Ad Valorem Insurance: This type of insurance compensates you "according to value" (which is what "ad valorem" means in Latin). You declare the actual value of your goods, and in the event of a claim, you are reimbursed on that basis.

It's the difference between receiving €5 for your lost smartphone and receiving its actual purchase price.

Basic Insurance vs. Ad Valorem: A Head-to-Head Comparison

Which Ad Valorem Insurance Should You Choose Based on Your Profile?

Find our interactive carrier insurance comparison tool here

- Are you an individual who occasionally ships valuable items? Your Carrier Ad Valorem option Carrier be sufficient, but compare its cost with that of a specialized insurer.

- Are you a retailer small business/SME)? A specialized insurer is the only viable solution. It protects your margin, your time, and your reputation. Automation via CMS connector is a huge productivity gain in managing your disputes .

- Do you ship luxury, high-tech, or second-hand items? Carriers often exclude these goods. Only a specialized insurer like Claisy will offer you adequate coverage (as with the leading vinyl resale platform Dwice) to insure your parcels.

- Are you a marketplace? Customer experience is essential, and so is protecting your sellers: discover how Claisy can revolutionize your protection of sellers and buyers - digitize your Dispute process.

Practical Checklist: Best Practices for the Insured Shipper

- Before shipping: Purchase insurance before shipping. Always keep the purchase invoice or proof of value for your item.

- Packaging: Use neutral, sturdy packaging. Never mention the nature or value of the contents on the parcel.

- In the event of a claim: Damaged parcel, Lost parcel, Lost parcel contents: Take photos (if damaged or stolen), contact your insurer immediately, and keep all documents (proof of deposit, email exchanges, etc.).

In conclusion, choosing ad valorem insurance does not mean "spending more." It means deciding to invest in the security of your property, your peace of mind, and the satisfaction of your recipients.