"Your parcel is on its way." Five words that should be synonymous with satisfaction. Yet for millions of shippers, they mark the beginning of a period of anxiety. Will the parcel arrive? In what condition? And if it is lost or stolen, who will pay for the damage?

By analyzing logistics flows and friction points in e-commerce, it quickly becomes clear that disputes impact shippers' profitability: the biggest mistake is therefore to believe that all shipments are equal. Insured parcel delivery is not just an option; it is a strategic decision that separates amateurs from professionals, those who suffer the risks from those who control them.

France market data for 2025:

- 2.3 billion parcels shipped

- Average loss ratio: 2-3% depending on sector

- Total cost of uninsured claims: €450 million/year (e-commerce SMEs)

- 35% of customers do not return after a bad experience (source: study)

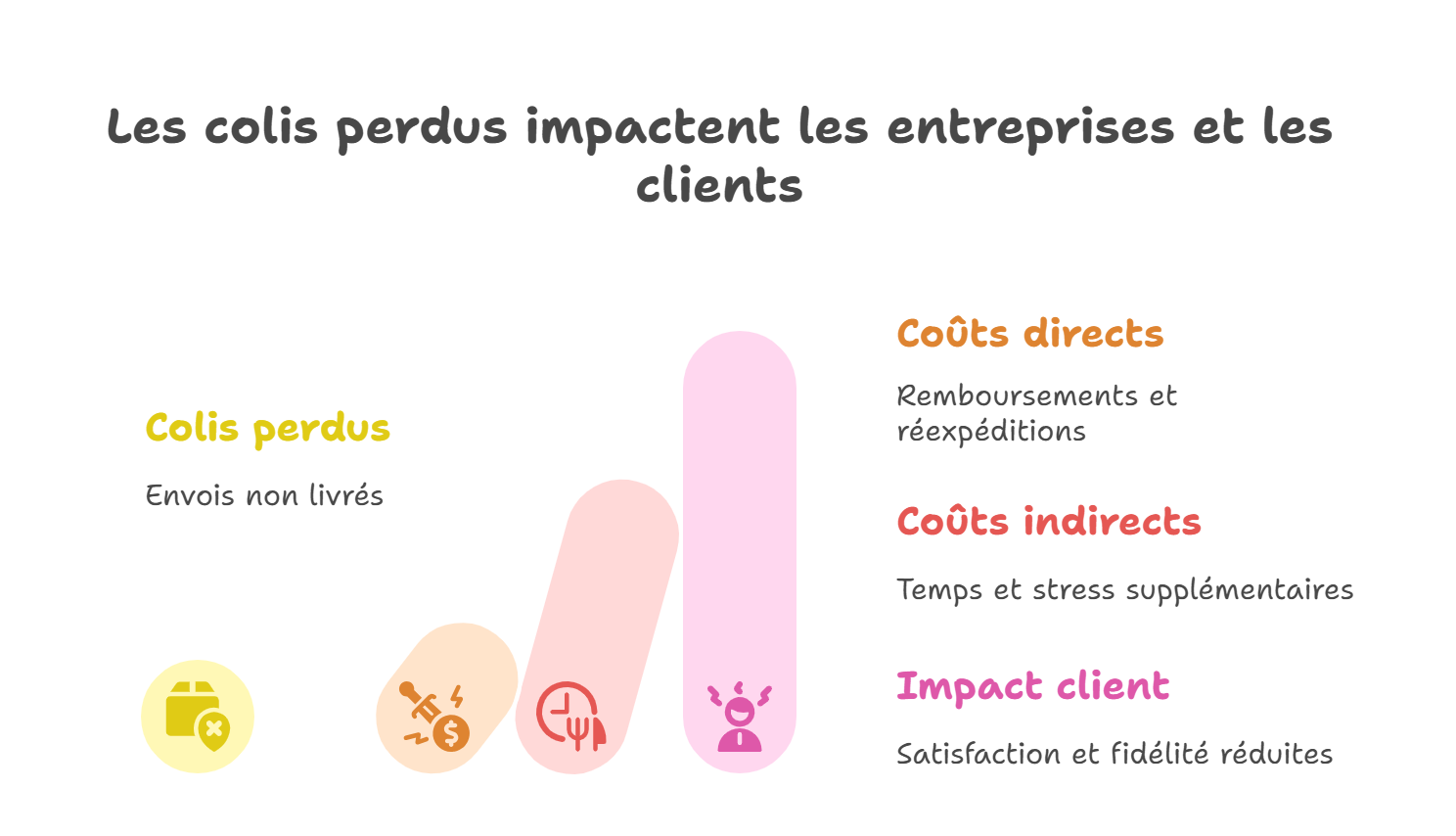

Detailed financial impact:

- Average cost of an e-commerce claim: €180 (shopping cart + reshipment + after-sales service time)

- Average cost of a B2B claim: €2,500 (critical part + production stoppage)

- Indirect impact: Customer lifetime value (CLV) loss = €50–€150

Actual Cost of Loss = Product Value + Reshipment Costs (€6-€15) + Customer Service Time (€15-€30) + Customer Impact (€50-€150)Example: Lost parcel worth €150 = €150 + €10 + €20 + €80 = €260 actual loss

This guide is not just a simple information page. It is your comprehensive roadmap for navigating the world of parcel insurance, understanding its pitfalls, and choosing the protection that will truly secure your money, time, and reputation.

Why Insure Your Parcel Delivery? The Harsh Reality of Transportation

The question is no longer "should you insure?", but "can you afford not to?". The explosion of e-commerce has automatically increased the risks and therefore raises the question of whether to send insured or uninsured parcels.

- The Numbers Don't Lie: Every year, millions of parcels are reported lost, damaged, or stolen. The total cost of these losses amounts to billions of euros for retailers alone.

- The Financial Impact: An uninsured parcel that gets lost is a double loss: the value of the merchandise AND the cost of reshipping. Your margin evaporates instantly.

- Impact on Reputation: Over 35% of customers will not recommend a site after a bad delivery experience. A Dispute handled Dispute means a lost customer for life and a potential negative review.

The Big Names in Parcel Insurance: Don't Fall Into the Trap

There are two radically different philosophies when it comes to parcel delivery insurance. Understanding this distinction is the first step in deciding whether or not to ship your parcels with insurance.

1. Basic Carrier Insurance: The False Good Idea

All carriers (Colissimo, Chronopost, etc.) include basic "insurance." Be careful, this is a trap.

- How it works: It is a flat-rate compensation, generally based on the weight of the parcel (e.g., €23/kg).

- The problem: For a 200g smartphone worth €1,000, you would be reimbursed... less than €5. It is illusory "protection," designed for low-value goods.

2. Delivery Insurance: The Only Real Protection

This is the standard for professional insurance. "Ad Valorem" means "according to value."

- How it works: You declare the actual value of your shipment, and you will be compensated on that basis in the event of a claim.

- The advantage: Whether your parcel contains jewelry, artwork, or high-tech equipment, its value is truly protected (subject to conditions).

3 existing models:

A. Ad Valorem Carrier Option):

- Cost: 1-3% of value

- Limits €5,000–10,000

- Exclusions: Numerous

- Compensation period Dispute : 60-90 days

B. Ad Valorem Platform (Sendcloud, Boxtal, Upela, etc.):

- Cost: Varies depending on partner

- Limits €5,000–20,000 (depending on partner)

- Compensation period for Dispute : 50-90 days

C. Specialized Ad Valorem (Claisy):

- Cost: 0.6-0.9% of value

- Limits €100,000

- Exclusions: Minimal

- Compensation timeframe Dispute : 48-72 hours

5 Key Points for Comparing Parcel Insurance Offers

Now that you know you need Ad Valorem insurance, how do you choose the right one? Here is your comparison checklist.

- Limit : How much are you actually covered for?

- Pricing and Business Model: Is the cost a fixed percentage of the value? Are there any hidden fees or subscription costs?

- Covered Items and Exclusions: Is your type of product (luxury, used, high-tech) explicitly covered? Read the fine print!

- Claims Management: Is the claims process quick and easy? Do you receive compensation within 72 hours or three months?

- The Target: Is the offer suitable for individuals, SMEs, or large volumes?

Comparison of the Best Parcel Delivery Insurance Policies

The market is divided into two camps: insurance offered directly by carriers and insurance offered by independent specialist insurers. For more details, please consult our comprehensive comparison of ad valorem insurance policies and focus on all parcel insurance offers on our hub (Carrier, CMS, Transport Broker, etc.).

The key differentiator: Specialized insurance solutions such as Claisy have built their model to fill all the gaps left by carriers and allow you to ship all your insured parcels, even when carrier insurance excludes your goods. Not only do they offer better coverage at a better price, but they also provide technological tools (connection to Shopify, PrestaShop, Magento, etc.) to fully automate parcel insurance management, which is impossible with carriers' offerings.

Which Parcel Insurance Should You Choose Based on Your Profile?

Find our interactive carrier insurance comparison tool here

- Are you an individual who occasionally ships valuable items? Your Carrier Ad Valorem option Carrier be sufficient, but compare its cost with that of a specialized insurer.

- Are you a retailer small business/SME)? A specialized insurer is the only viable solution. It protects your margin, your time, and your reputation. Automation via CMS connector is a huge productivity gain in managing your disputes .

- Do you ship luxury goods, high-tech items, or secondhand goods? Carriers often exclude these items. Only a specialized insurer like Claisy will offer you adequate coverage to insure your parcels.

- Are you a marketplace? Customer experience is essential, and so is protecting your sellers: discover how Claisy can revolutionize your protection of sellers and buyers, digitize your Dispute process.

Practical Guide: How does Delivery Insurance work?

The Declaration of a Dispute

Be sure to check the eligibility requirements and Dispute procedures. At Claisy, the conditions are simple: for orders over €1,000, delivery must be made with a signature AND there must be no indication of value on the outside of your parcel (including on the shipping label)!

Next, if a Dispute arise, here are the four key areas where you should focus your efforts:

- Respect the deadlines! You generally have 48 to 72 hours after delivery to report damage or theft, and a longer period (e.g., 30 days) for loss.

- Gather evidence: Purchase invoice, proof of shipment, photos of damage, sworn statement, Filing a police report necessary.

- Submit your claim on your insurer's platform.

- Follow up on the claim and wait for compensation. A good insurer will reimburse you within a few days, not a few months.

To learn more about disputes management disputes Claisy, click here.